Bahrain banks ‘resilient’

MANAMA: Bahrain’s banking sector remains resilient in challenging times with robust assets growth and liquidity ratios, according to a KPMG report.

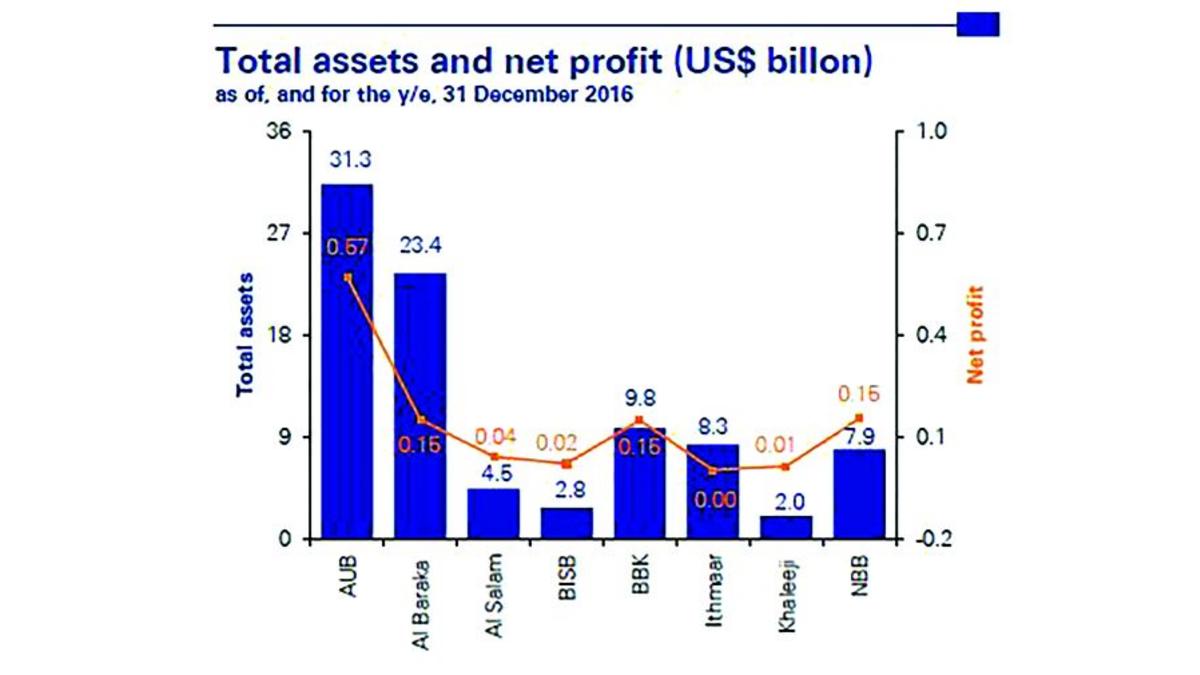

The key takeaway from the GCC listed bank results report – which analyses the published 2016 financial statements of 56 leading listed commercial banks across Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE – is that the overall outlook for the GCC’s banking sector is positive and Bahrain is faring particularly well.

The report, which covers more than 90 per cent of the region’s listed banking assets, indicates that banks have performed well over the 12 months till December 2016 in light of margin compressions, increased impairment charges and increased funding costs.

“Despite the challenging economic conditions in the region which led to a year-on-year decline in net profit for the first time in recent years, asset growth remained robust at 6.5pc on average across the region,” KPMG in Bahrain partner and head of financial services Jalil Al Aali told the GDN.

“The annual growth in Bahrain’s financial services sector has been strong, from 1.7pc in 2015 to 7.4pc as of the third quarter in 2016.

“However, due to a sharp decline in lending to cer

tain sectors, credit growth in Bahrain experienced renewed slowdown with peaks recorded around the beginning of 2016.

“Profit declines were predominantly due to margin pressure but on a positive note, cost to income ratios continue to decline reflecting significant focus on cost reduction and operational efficiency,” he added.

“Such challenges are making banks seek innovative ways to stay ahead.”

The report finds that banks in Bahrain are in a “very strong position to weather the current economic and political challenges, giving the expectation of continued government support and committed infrastruc

ture investment which will help maintain stability in the sector”.

Return on assets – an indicator of how profitable a company is relative to its total assets – was at 1.3pc and return on equity, the amount of net income returned as a percentage of shareholders equity, was 6pc.

The capital adequacy ratio, a measure of a bank’s capital, for the sector as a whole increased to 19.2pc during the year and profitability of the banking sector increased.

The challenge for banks was to keep the impaired loans in check after a slight increase due to two major sectors – manufacturing and mining.

According to Mr Al Aali, the industry’s current focus is to improve on profitability with quality asset growth through innovation and collaboration.

“Technology advancement, high Internet and smartphone penetration rates all mean that digital banking is the future.

This puts emphasis on innovative customised products and pricing to improve the banking capabilities and meet the expectations of today’s tech-savvy customers,” he said.

The report also notes that changing global regulatory requirements have had an impact on banking in the GCC with a number of positive changes being made to bring banks in line with new requirements.

GCC banks are highly capitalised to withstand a slowdown in the economy, says KPMG.

“Capital adequacy ratios now stand at over 18pc across the region – above the minimum limits set in Basel III, reflecting effective capital raising activity,” said Mr Al Aali.

“Similarly, Basel III requirements are the likely reason for a rise in liquidity ratios across most countries, demonstrating a commitment to adhere to broader global regulations.”

The KPMG assessment, however, says that key challenges facing banks remain being profitable while managing the quality of the loan portfolio and pressure on margin due to increased competition and increased cost of funding.